Who are the innovators, MFIs or commercial banks?

Digital products and services are often assumed to be driven by MFIs. However, commercial banks find these relevant as well.

Since the inception of microcredit in the 1970s, its business model has seen a number of shifts: in the nineties, the concept of microcredit evolved into a more commercially sustainable microfinance, which included savings. Early 21st century, the financial inclusion paradigm led to further commercialisation and a wider understanding of the industry, which now included commercial banks serving low-income clients.

Today, we stand witness to a third revolution: digitalisation. New products and channels promise better service and larger outreach, digital field automation allows for unprecedented levels of efficiency, and new players promise a range of potential competitors and partners.

Today, financial institutions worldwide need to digitalise in order to stay competitive.

How far have they come, and how far are they willing to go? Those are

the questions BIO set out to answer with its comprehensive screening of

its financial institutions portfolio in Africa, Asia and Latin America

(The survey covers financial institutions in BIO’s portfolio. Based

on

its sample size, it is not representative for the entire industry.)

With the help of PhB Development, BIO collected information on the

strategic priorities and challenges of financial institutions and on the

level of digitalisation. The survey covered the digital products and

services offered by each institution, the level of digitalisation of

internal processes and the technological readiness for digital

innovation. It also included digital partnerships (such as with Mobile

Network Operators, agent networks, FinTechs and others) and it covered

the clients’ attitude towards digital products and services and their

uptake.

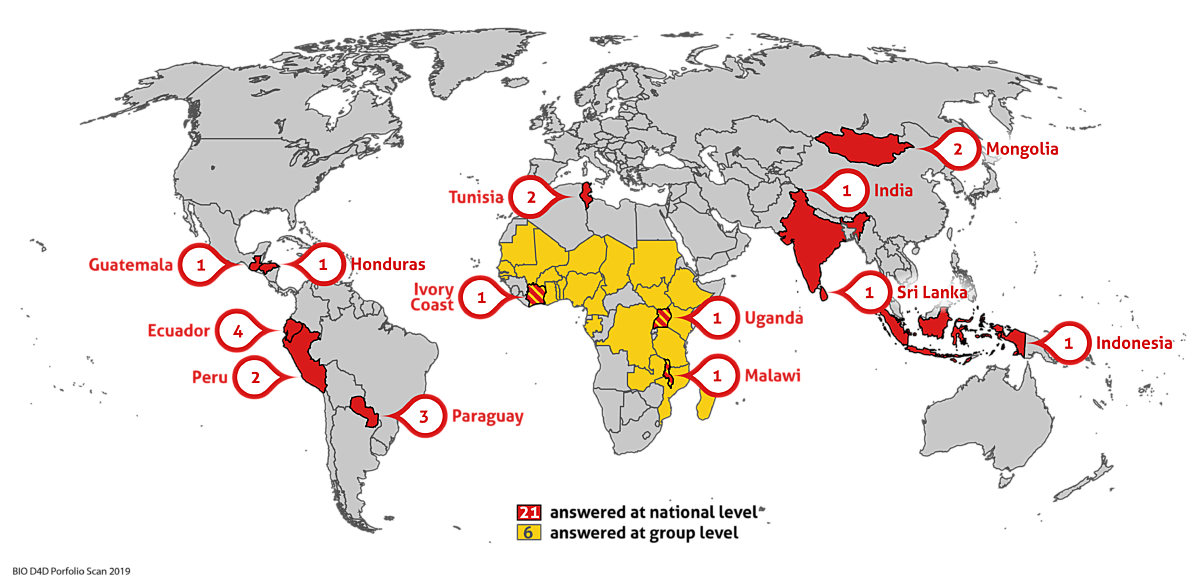

Geographic location of BIO investees surveyed

Methodology

A total of 27 financial institutions in BIO’s portfolio, including

microfinance institutions (MFIs), non-bank financial institutions, and

commercial banks, participated in this study.

The online survey was available in English, French and Spanish and was followed by personal interviews. On some clients, BIO provided in-house information.

We would like to extend a warm thank you to the team of PhB Development as well as to all our clients who took the time to participate in the study and share insights into their digitalisation process.

Reaching out to the poor and to rural areas, digitalisation is often associated with MFIs

Digital products and service offerings such as mobile banking, digital loans, or agent banking are often assumed to be driven by microfinance institutions (MFIs), as the benefits of digitalisation for financial inclusion are clear: with a lower-touch model, MFIs can reach out to more clients. They can reach into rural areas that were previously considered unbankable. They can offer their services at a much lower cost, enabling them to work with poorer and more remote customers.

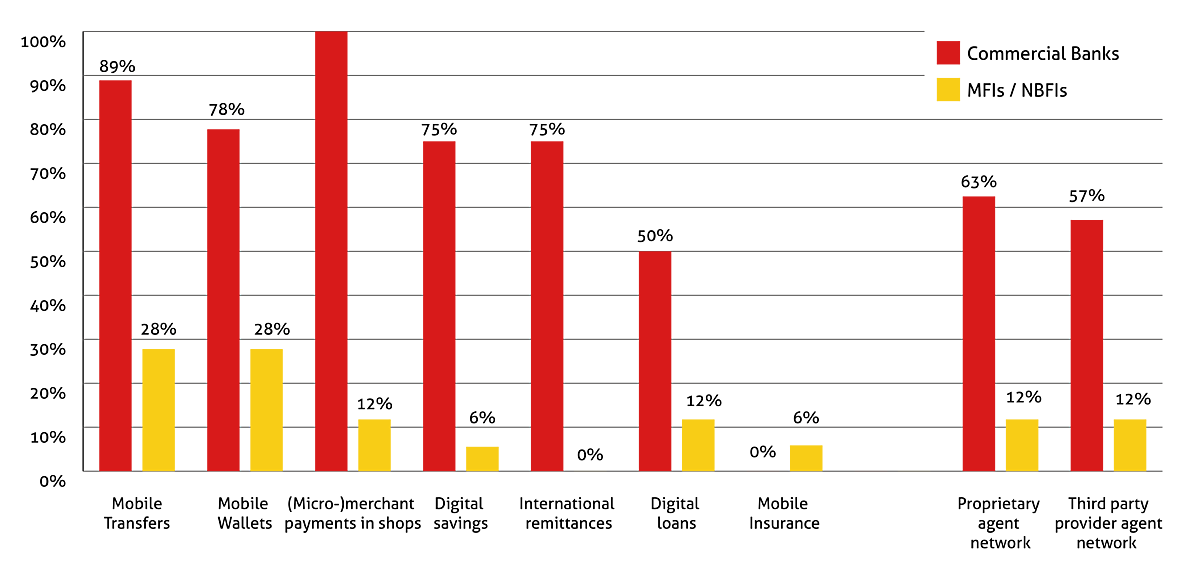

However, commercial banks find digital financial services relevant as well. These banks address both the SME market as well as higher-income retail clients and large corporates– and they have deeper pockets. Digitalisation has become important for customer convenience and efficiency. The results of the survey show how far commercial banks have advanced in this regard - in many instances, they are the real innovators and drivers of mobile banking, digital loan products, and agent banking services.

The real champions of digitalisation are commercial banks

In our survey, to avoid distortions caused by differences in regulatory environments, we separated institutions by business model rather than by license, i.e. an institution fully focusing on the microfinance target market but operating with a banking license is considered an MFI. We obtained a group of large commercial banks with a full-fledged banking offer, including a relevant amount of SME lending. The second group consists mainly of MFIs; plus a low number of non-bank financial institutions (NBFIs) that are SME leasing companies and do not distort our findings.

Looking at the digital products and services offered by larger commercial banks compared to MFIs, the former are much more advanced in offering almost any type of digital product (except for generally undeveloped mobile insurance products). From mobile wallets to digital loans, commercial banks are ahead of MFIs. While we do not publish graphs on the different types of MFIs due to the limited sample size, the difference holds for all types: both deposit-taking MFIs and credit-only MFIs lag behind banks with their digital product offer.

There are some innovations that are more specific to low-income financial inclusion and rural outreach. Surely, you would expect MFIs to take the lead when it comes to agency banking? As it turns out, they do not. Commercial banks are much more likely to have a proprietary agent banking network than any other type of financial institution in our sample. They are also more likely than any other type to cooperate with third party agent networks to gain additional outlets for their clients.

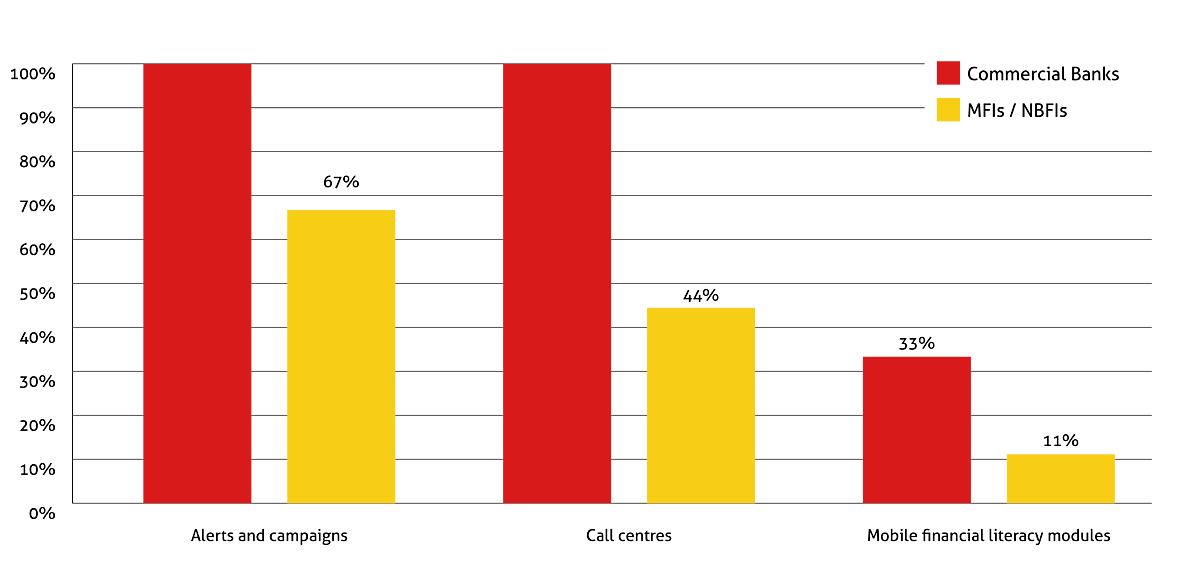

This message holds true when we look at digital communication channels with clients. Unsurprisingly, the banks more frequently offer call centres. But they also prevail when it comes to using digital communication channels for client alerts or marketing campaigns. Perhaps this is due to the cost of these commercial offers? Perhaps the MFIs are more focused on impact-related communications such as financial literacy? Not when we look at digital offers: while 27% of commercial banks in our sample offer mobile financial literacy modules, only 13% of the MFIs do.

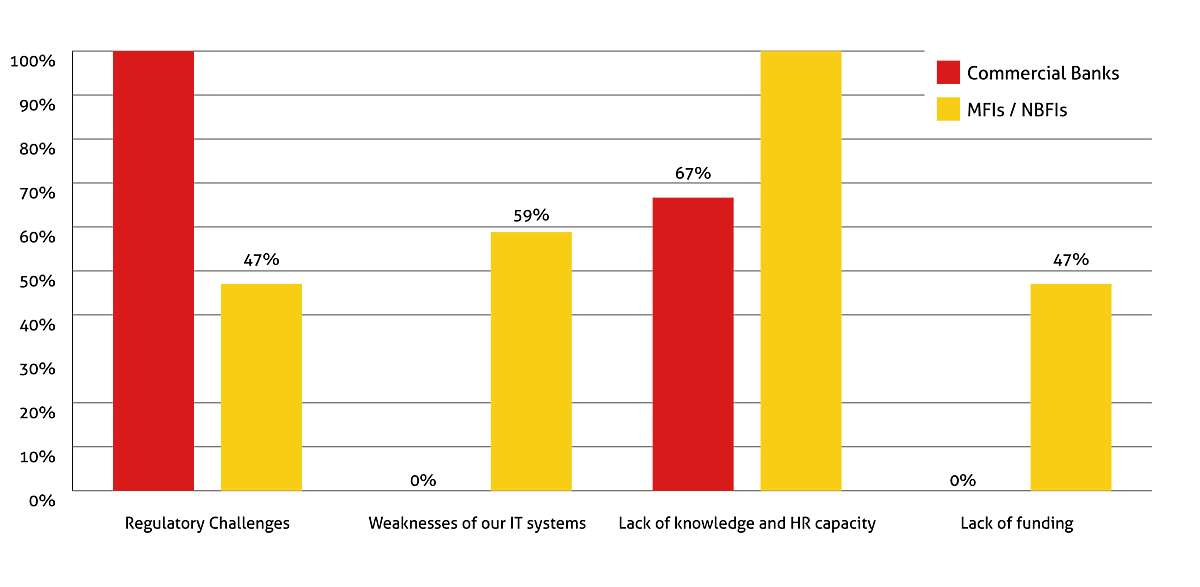

MFIs are held back by legacy IT systems and a lack of funding

One of the reasons for this divide between commercial banks and MFIs becomes apparent from the challenges that financial institutions face in relation to digitalisation. MFIs collectively cite an enormous gap of knowledge and lack of skilled staff to manage the challenges of digitalisation. 59% also highlight the weaknesses of their IT system as a major challenge. Almost half of them struggle with a lack of funding for digitalisation; funding necessary to address the skill gap or upgrade information technology. These are basic barriers that tend to slow down even the most simple steps of the digitalisation process.

Banks mostly struggle with regulatory challenges and, to a lesser extent, with skill gaps amongst their employees. They are more heavily regulated than MFIs in most markets. And regulation is less of a challenge for basic digitalisation and more so for advanced levels of digitalisation, leading to real innovation outside the usual business model. IT systems and funding do not play a role - it seems that banks have reached their higher level of digitalisation with sufficiently strong IT systems, able to handle more complexity and connectivity. Banks have funds at their disposal to support big digitalisation projects and to hire expertise in their local markets. Ultimately, digitalisation seems a game of scale.

Tailored support will be needed to help MFIs succeed in a digitalised world

To counter the challenges MFIs face to keep up with the sector’s pace of digitalisation, BIO is working on the creation of technical assistance programmes to support them. We will focus our financial support on MFIs that require help to enter the era of digital finance and are facing funding constraints.

We now have detailed insights into where our clients stand, what they need to further digitalise, and how interested they are in digitalising with grant support. Based on that, BIO is currently selecting the first MFIs to support on their digitalisation journey.

We will help these institutions address the biggest challenges that our survey has identified: While knowledge challenges can be addressed by traditional forms of technical assistance (TA) which support the input of consultants and trainers, BIO has recently amended its TA guidelines to also support selected IT projects, which would allow institutions to speed up their digitalisation processes.

Definitions

Alerts and Campaigns

Using SMS and other digital notifications to communicate with your clients (be it on repayment/savings schedule, marketing, etc.)

Call centres

Answering clients queries via a dedicated team and/or chatbot

Deposit & Withdrawal on mobile wallets

The possibility to make deposits and withdrawals using a mobile wallet via branches/agents

Digital Financial Services

Refers to financial services provided to clients through alternative distribution channels (mobile, internet, agents) that have developed over the past 10-15 years.

Digital loans

The possibility for clients to apply and obtain a loan via a mobile application and without having to visit a branch

Digital savings

The possibility for clients to open and contribute to a savings account directly from their mobile phone without visiting a branch

Financial institutions

Refer to banks, microfinance institutions and other forms of formal financial institutions that provide financial service to clients. They do not include mobile network operators or FinTechs.

International remittances

The possibility to send and receive funds from other countries digitally

(Micro-)merchant payments in shops

The possibility for clients to make small value payments to merchants using digital tools (NFC, QR code, or USSD and POS)

Mobile banking

Clients perform banking transactions themselves using their mobile phones (loan repayment, balance and statement request, etc.)

Mobile Financial Literacy

Modules Using mobile phones or tablets to educate our clients

Mobile Insurance

An insurance scheme that is offered via mobile

Mobile transfers

The possibility for our clients to transfer funds from their bank account to their mobile wallet/other people's mobile wallets or bank accounts and vice-versa

Proprietary agency banking

Digital financial services provided via the financial institution's own network of retail agents (branded under the financial institution’s logo/service name).

Third-party provider agent network

Digital financial services provided via a network of existing retail agents that are managed and branded under a third party's logo/service name.