The hidden pitfalls of digitalisation

Innovation comes with risks for financial inclusion

Since the inception of microcredit in the 1970s, its business model has seen a number of shifts: in the nineties, the concept of microcredit evolved into a more commercially sustainable microfinance, which included savings. Early 21st century, the financial inclusion paradigm led to further commercialisation and a wider understanding of the industry, which now included commercial banks serving low-income clients.

Today, we stand witness to a third revolution: digitalisation. New products and channels promise better service and larger outreach, digital field automation allows for unprecedented levels of efficiency, and new players promise a range of potential competitors and partners.

Today, financial institutions worldwide need to digitalise in order to stay competitive.

How far have they come, and how far are they willing to go? Those are the questions BIO set out to answer with its comprehensive screening of its financial institutions portfolio in Africa, Asia and Latin America (The survey covers financial institutions in BIO’s portfolio. Based

on its sample size, it is not representative for the entire industry.) With the help of PhB Development, BIO collected information on the strategic priorities and challenges of financial institutions and on the level of digitalisation. The survey covered the digital products and services offered by each institution, the level of digitalisation of internal processes and the technological readiness for digital innovation. It also included digital partnerships (such as with Mobile Network Operators, agent networks, FinTechs and others) and it covered the clients’ attitude towards digital products and services and their uptake.

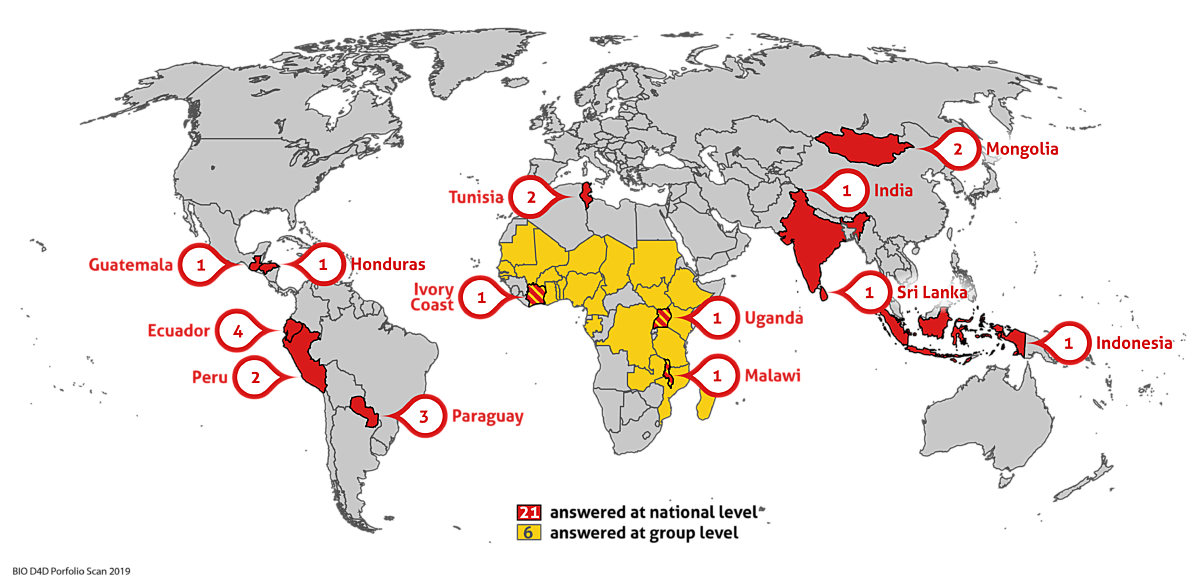

Geographic location of BIO investees surveyed

Methodology

A total of 27 financial institutions in BIO’s portfolio, including microfinance institutions (MFIs), non-bank financial institutions, and commercial banks, participated in this study.

The online survey was available in English, French and Spanish and was followed by personal interviews. On some clients, BIO provided in-house information.

We would like to extend a warm thank you to the team of PhB Development as well as to all our clients who took the time to participate in the study and share insights into their digitalisation process.

Digitalisation is the top priority: (almost) everyone is doing it

The results are impressive: All institutions in the sample are either already offering digital financial services to their clients (78%) or planning to (22%), with the “planning stage” referring to concrete products currently under development. Most of those in the planning stage are aware that they are lagging behind and the remainder are leasing companies, which face less pressure to innovate. Similarly, all institutions are either already using digital tools to enhance operational processes (75%) or concretely planning to (25%).

The urgency to digitalise has reached all types of financial institutions. While many digital products, channels and services are still under development, the message is clear: digitalisation concerns everyone. Some speak about a “necessity to digitise”, others call on MFIs to “digitise or die”. In the interviews, BIO’s clients presented digitalisation as a matter of survival.

Surprisingly often, the foundations for digitalisation are lacking

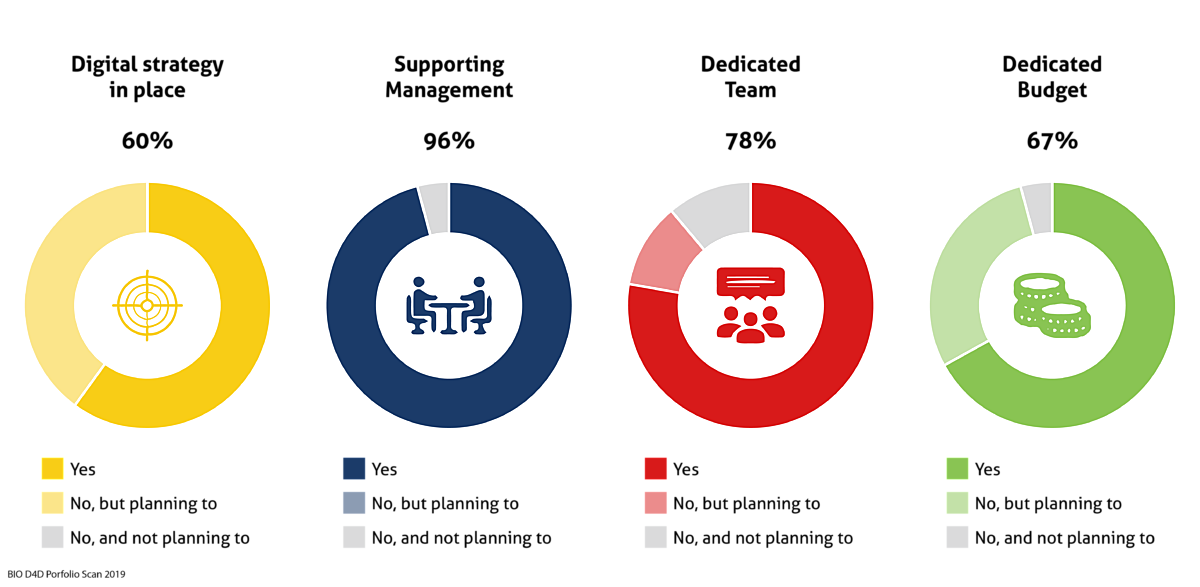

Strikingly, not many institutions have the basic enablers for digitalisation in place. While almost all institutions have a supportive management that has recognised the importance of digitalisation, 22% do not have a dedicated staff or team and 33% do not have a dedicated budget, even though almost all of them do see the need.

Most noteworthy is that while everyone has rushed to introduce elements of digital innovation to their companies, not everyone knows where they are headed: 40% of the respondents do not have a digitalisation strategy in place. They have started on their journey without a strategy and are planning to come up with one along the way. This is rather concerning, given that digitalisation profoundly changes the functioning of a financial institution and touches on almost all products and services, redefining its client relationships, changing its operating processes and involving almost every department in the institution.

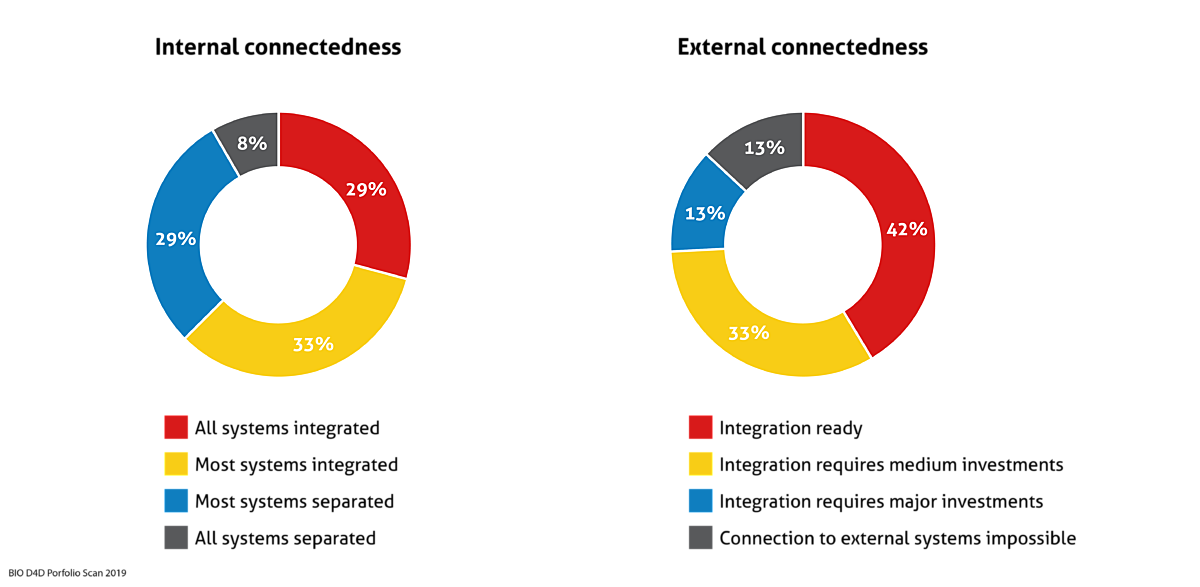

Similarly, introducing digital products, services or tools is not always supported by technological readiness. More than a 3rd of financial institutions operate with most or all of their IT systems separated (e.g.; Management Information System, HR systems, financial reporting systems) and only 29% have managed to integrate all of them. With regards to connecting to systems of outside providers or partners (e.g. FinTechs, clearing houses, telecommunication operators, agent network managers), the situation is only slightly better: 13% of respondents have Management Information Systems that cannot be connected to third party systems. For others, integrations would require major (13%) or medium sized (33%) investments. Only 42% of financial institutions have integration-ready Management Information Systems.

It seems that, at least for some institutions, the achieved digitalisation is only superficial. Given the pressure of the market and in the industry in general, the incumbents in the financial institution space rush to quickly introduce a digital product or channel, to add a digital tool here or there. However, many have no idea where their digital journey is supposed to take them, with no digital strategy to guide their choices and priorities in a rapidly evolving environment. Nor have they managed to achieve the technological level necessary for successful digitalisation in the long run.

Based on these findings, BIO is working on the creation of technical assistance programs for selected clients to support them with digitalisation. We will identify the most urgent needs and work with those clients most ready to benefit from our support. As it stands, a digitalisation strategy should probably be a priority item on the agenda.

At the same time, the results of this survey may serve as a warning to the industry: innovation done fast is not always innovation done well. Putting excessive pressure on investees, subsidiaries or business partners to digitalise may put institutions at risk. And this ultimately means putting clients and their financial inclusion at risk.

Digitalisation is of the utmost importance and the associated urgency for financial service providers is real. However, to succeed in the long-run, financial institutions should follow realistic plans, taking into account both their capacities and their clients’ needs.

Definitions

Digital Financial Services

Financial services provided to clients through alternative distribution channels (mobile, internet, agents) that have developed over the past 10-15 years.

Digital loans

The possibility for clients to apply and obtain a loan via a mobile application and without having to visit a branch

Financial institutions

Banks, microfinance institutions and other forms of formal financial institutions that provide financial service to clients. Mobile network operators or FinTechs are not included.

International remittances

The possibility to digitally send and receive funds from one country to another country

Management Information System - MIS

The entire back-office system, including portfolio management and reporting. Broader than a core banking system, which is limited to capturing and processing data.

Mobile banking

Banking transactions performed by clients themselves using their mobile phones (loan repayment, balance and statement request, etc.)

Mobile transfers

The possibility for clients to transfer funds from their bank account to their mobile wallet/other people's mobile wallets or bank accounts and vice-versa