Benchmarks on digitalisation

Since the inception of microcredit in the 1970s, its business model has seen a number of shifts: in the nineties, the concept of microcredit evolved into a more commercially sustainable microfinance, which included savings. Early 21st century, the financial inclusion paradigm led to further commercialisation and a wider understanding of the industry, which now included commercial banks serving low-income clients.

Today, we stand witness to a third revolution: digitalisation. New products and channels promise better service and larger outreach, digital field automation allows for unprecedented levels of efficiency, and new players promise a range of potential competitors and partners.

Today, financial institutions worldwide need to digitalise in order to stay competitive.

How far have they come, and how far are they willing to go? Those are

the questions BIO set out to answer with its comprehensive screening of

its financial institutions portfolio in Africa, Asia and Latin America

(The survey covers financial institutions in BIO’s portfolio. Based

on

its sample size, it is not representative for the entire industry.)

With the help of PhB Development, BIO collected information on the

strategic priorities and challenges of financial institutions and on the

level of digitalisation. The survey covered the digital products and

services offered by each institution, the level of digitalisation of

internal processes and the technological readiness for digital

innovation. It also included digital partnerships (such as with Mobile

Network Operators, agent networks, FinTechs and others) and it covered

the clients’ attitude towards digital products and services and their

uptake.

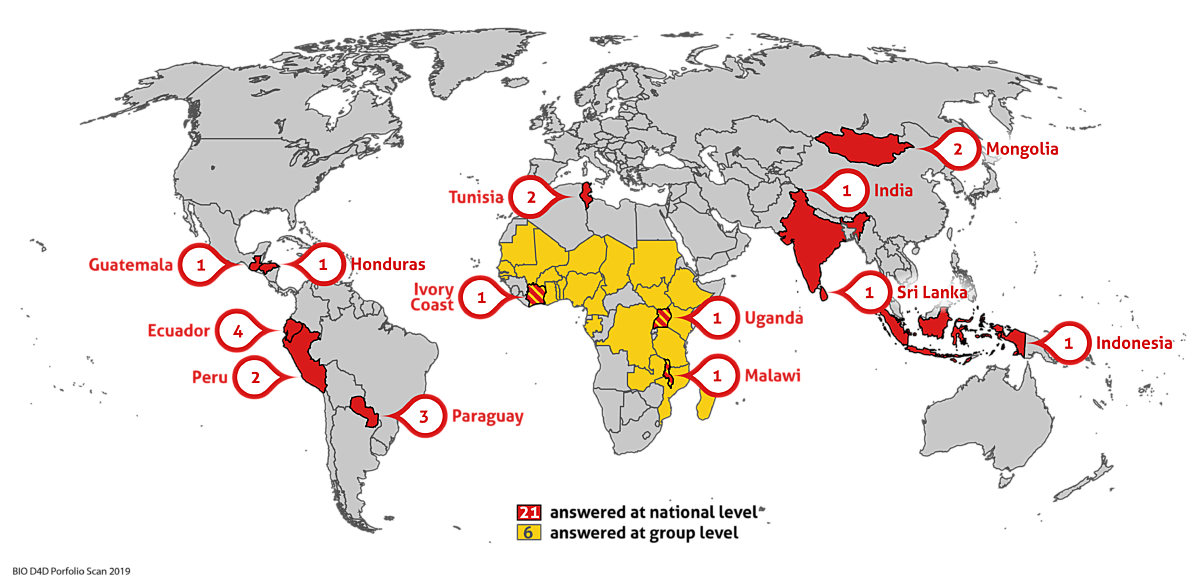

Geographic location of BIO investees surveyed

Methodology

A total of 27 financial institutions in BIO’s portfolio, including microfinance institutions (MFIs), non-bank financial institutions, and commercial banks, participated in this study.

The online survey was available in English, French and Spanish and was followed by personal interviews. On some clients, BIO provided in-house information.

We would like to extend a warm thank you to the team of PhB Development as well as to all our clients who took the time to participate in the study and share insights into their digitalisation process.

Digitalisation - Strategic priority number one

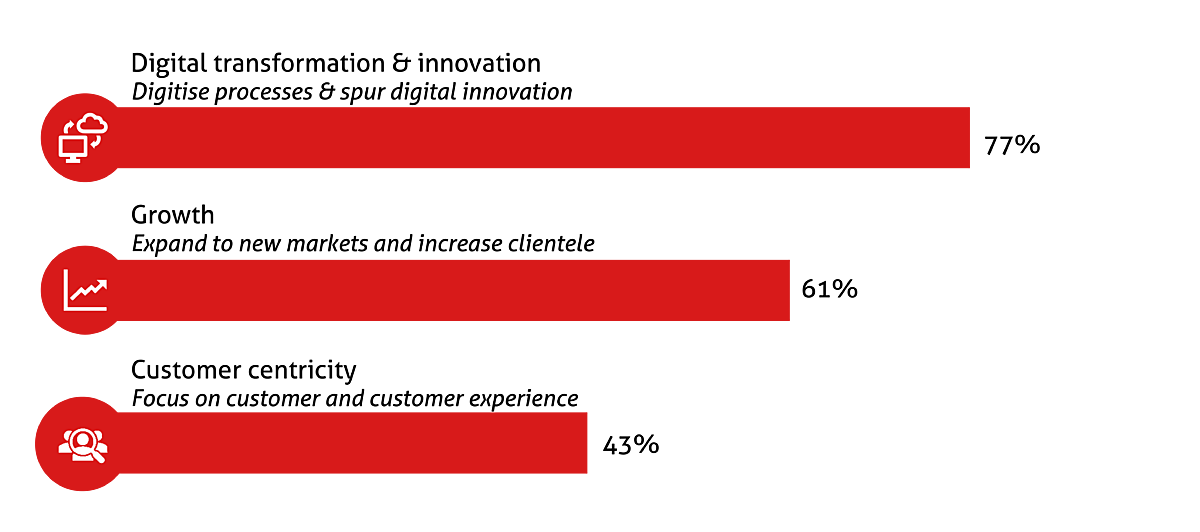

Digitalisation has become a strategic priority of BIO’s financial institution investees, with 77% of them mentioning digitalisation as one of their top three priorities. This message was very clear as well throughout the qualitative interviews following the survey: many respondents even went so far as to describe digitalisation and digital transformation as a matter of survival. This is shared by both operations teams and top management: in almost all institutions (96%), top management actively supports the digitalisation process.

Ranking of strategic priorities:

Respondents were asked to list their top three strategic priorities, without being provided a list of suggestions. Percentages indicate the frequency a topic was mentioned in the top 3, i.e. 77% of respondents mentioned digitalisation as one of their top three strategic priorities.

A second priority is growth and expansion (61%), of which digitalisation can be an important ingredient. The third most frequently mentioned strategic priority is customer centricity (43%). Putting customer interests at the centre is increasingly acknowledged as fundamental to achieve impact, but also growth and commercial success. It is an important ingredient for successful digitalisation as well.

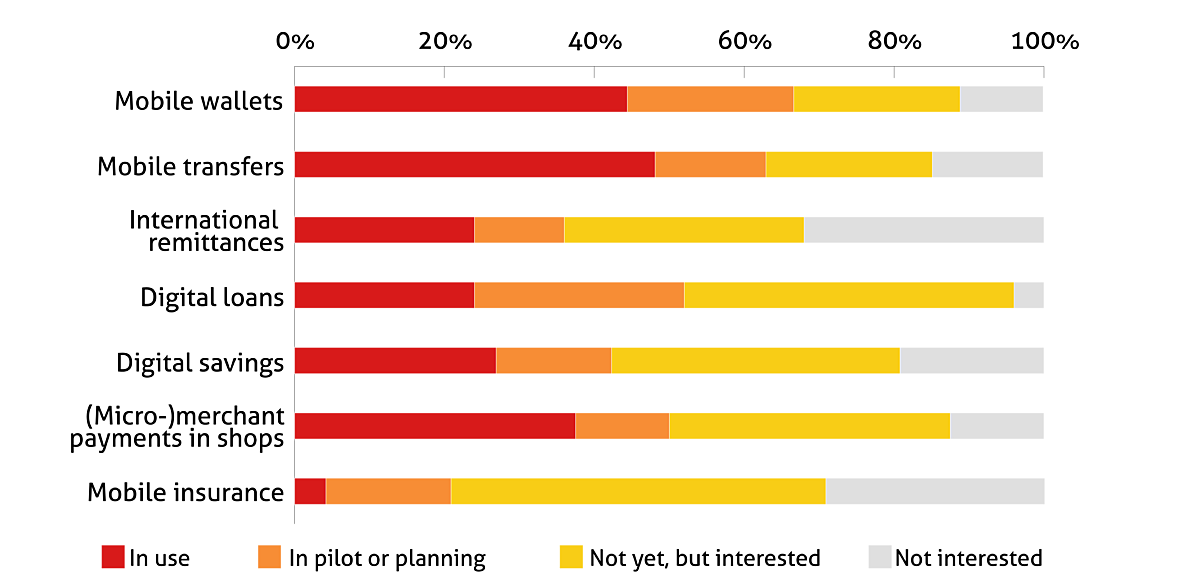

Mobile wallets and transfers are the most common digital channels

Many of our clients wonder how they compare to competitors in terms of digitalisation and what digital products and channels they should start with. In a recent report, we published a breakdown of the digital offer of our MFI and bank clients. But most have bigger ambitions, and many respondents already have concrete digitalisation projects on their way as well as a high level of interest in further digital developments.

The most common starting point for BIO’s clients are mobile wallets for deposits and withdrawals and mobile transfers. A majority of the respondents (>60%) already offer one or both of these products or are concretely working on their introduction. However, about 30-40% of financial institutions do not and will not do so in the near future. This is not due to a lack of interest, but rather due to challenges on the path to implementation. The 10-15% of institutions that are not interested are almost exclusively financial institutions that do not (and cannot) offer deposit and transaction products.

Digital product landscape

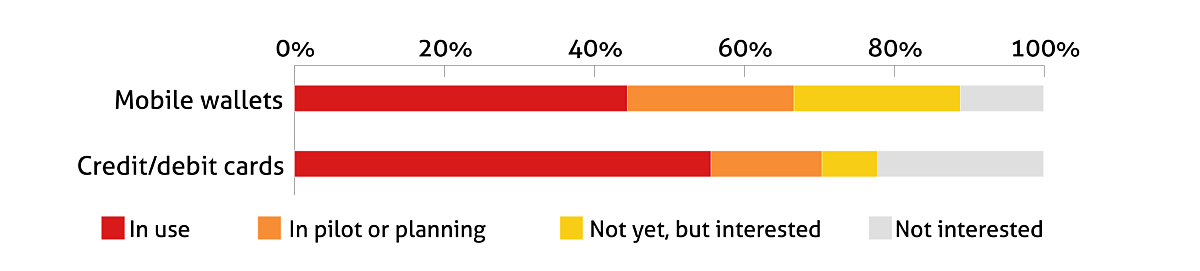

To compare the mobile channels to a more traditional form of remote access banking services, we also asked about the prevalence of credit cards. Being widely offered by commercial banks, but very little by MFIs, credit cards are now at a comparable level to mobile wallets: while 67% of institutions are offering or introducing mobile wallets, this is true for 70% with credit cards. The fact that some institutions are still working on the introduction of credit cards shows that these have not yet been replaced by mobile channels. That said, this will likely happen in the future – the share of institutions not interested in offering credit cards (22%) is double those not interested in mobile wallets (11%).

Mobile access versus card access

Interestingly, while less discussed in the industry, merchant payment services – allowing clients to make digital payments to merchants – are already widely offered as well (38% in use, 13% being introduced, totalling half of all surveyed institutions). Finally, mobile insurance is the least common digital product, offered by only 4% of institutions. Although there seems to be some potential going forward (17% are already introducing mobile insurance products while 50% would be interested in doing so), almost 30% of financial services providers see no interest in offering mobile insurance products. This might be because, even as a traditional, non-digital product, insurance is not an easy business case and not offered by many financial institutions.

Digital credit - Hype & criticism

While sometimes portrayed as the long awaited solution to expand the access to credit, especially to remote areas, and to reduce the costs of loans, there has been a growing debate on the potential dangers of digital credit (i.e. loans obtained without visiting a branch). Digital loans have come under increasing criticism for over-indebting customers, for enabling alcohol consumption and betting and for getting borrowers blacklisted with credit bureaus for tiny amounts, excluding them from future credit by destroying their credit history. In addition, there are the aggressive collection practices of certain providers of digital credit.

If we look at the financial institutions in our sample, less than a quarter offer digital loans. However, out of all the digital products and channels, digital loans do enjoy the highest level of interest. Only 4% of financial services providers are not interested in providing digital credit to their clients. Moreover, in addition to fully digital credit products, 56% of respondents have started to introduce digital elements to their traditional credit processes.

BIO’s clients seem to be aware of both the high potential of digital lending, and of its risks and challenges. They approach digitalisation gradually, postponing automated lending to a later phase. Hopefully, this will enable them to manage both the credit risk for the provider, as well as the risks for the customer, so that digital loans can grow out of their early-stage challenges before they get widely prevalent.

Note: Automatic loan renewals for repeat clients tend to be an entry step to digital credit. They come with tangible business potential and convenience benefits for customers while being easier to implement and lower risk than fully digital credit to new customers.

Digital client relationships

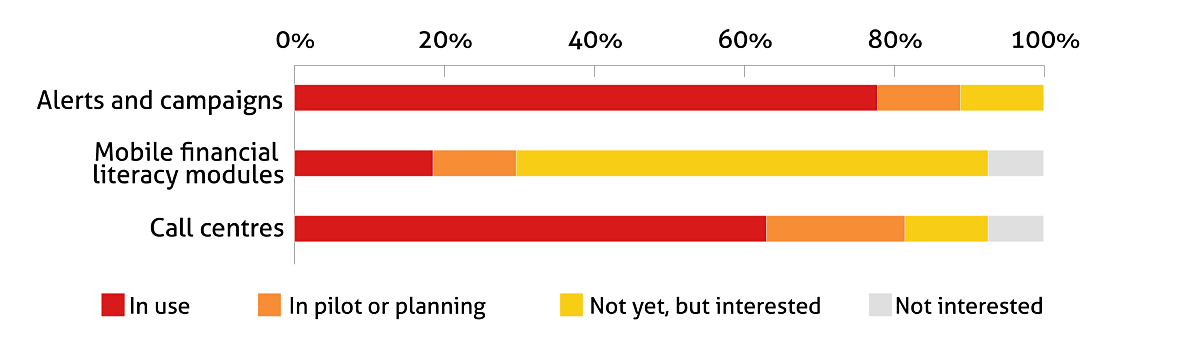

Last but not least, digital products and channels tend to be surrounded by digital client communication. The physical, close relationship with clients is being replaced or complemented by a digital, remote alternative. 78% of respondents actively offer digital notifications to their clients, be it deposit receipts to their phone, notifications of transactions, sms reminders of repayment deadlines, or simply for marketing messages. An additional 11% are actively introducing digital alerts and campaigns, and there is not a single institution, independent of business model, that is not interested in digital communication channels (this is particularly poignant when taking into account that this data was collected just prior to the start of social distancing measures under the covid 19 pandemic).

With most digital products and channels requiring 24h support, financial institutions need to be reachable for clients around the clock for troubleshooting. 63% of respondents offer call center support to clients, with another 19% in the process of introducing one.

Landscape of digital services

As they embark on their digitalisation journey and introduce new products and channels, financial institutions should not overlook the infrastructure that needs to be in place to offer quality service to their customers. 24/7 call centers can be a challenge to MFIs that were used to 9-to-5 working hours and that neither have Management Information Systems working day and night, nor staff. The good news is that this investment, once made, will be of use for all future steps of digitalisation. In addition, proactive call centers that reach out to clients for market surveys, measuring and improving customer satisfaction, enhancing the usage of deposit and transaction products, and for auditing purposes, can provide substantial benefits that go beyond trouble shooting for digital channels.

The picture looks different for Mobile Financial Literacy Modules. Less than 30% of respondents are running or introducing apps for clients to improve their financial literacy, using their phone. Where learning outcomes are required, personal interaction seems to be particularly difficult to replace by digital means. For mobile literacy trainings to succeed, a high level of client uptake, reading skills and digital literacy are likely a prerequisite, and may be just as difficult to achieve in many markets as financial literacy itself.

Given that almost 2/3rds of the financial institutions are interested in mobile financial literacy, however, it is likely that we will see more use of these modules going forward, in particular for younger target groups, which possess sufficient digital knowledge, but lack understanding of financial concepts. Still, it is unlikely that mobile applications will fully replace the traditional literacy trainings of MFIs any time soon. In fact, this is a good reminder that digitalisation is not a one size fits all approach, nor a goal in and of itself. Every financial services provider needs to identify the areas where they and their clients can benefit from the advantages of digitalisation. They need to carefully weigh in which areas personal contact with clients is preferred or even irreplaceable and in which areas digitalisation should remain limited to increasing the efficiency of background processes – supporting, rather than replacing human relationships.

Definitions

Alerts and Campaigns

Using SMS and other digital notifications to communicate with your clients (be it on repayment/savings schedule, marketing, etc.)

Call centres

Answering clients queries via a dedicated team and/or chatbot

Deposit & Withdrawal on mobile wallets

The possibility to make deposits and withdrawals using a mobile wallet via branches/agents

Digital Financial Services

Refers to financial services provided to clients through alternative distribution channels (mobile, internet, agents) that have developed over the past 10-15 years.

Digital loans

The possibility for clients to apply and obtain a loan via a mobile application and without having to visit a branch

Digital savings

The possibility for clients to open and contribute to a savings account directly from their mobile phone without visiting a branch

Financial institutions

Refer to banks, microfinance institutions and other forms of formal financial institutions that provide financial service to clients. They do not include mobile network operators or FinTechs.

International remittances

The possibility to send and receive funds from other countries digitally

(Micro-)merchant payments in shops

The possibility for clients to make small value payments to merchants using digital tools (NFC, QR code, or USSD and POS)

Mobile banking

Clients perform banking transactions themselves using their mobile phones (loan repayment, balance and statement request, etc.)

Mobile Financial Literacy

Modules Using mobile phones or tablets to educate our clients

Mobile Insurance

An insurance scheme that is offered via mobile

Mobile transfers

The possibility for our clients to transfer funds from their bank account to their mobile wallet/other people's mobile wallets or bank accounts and vice-versa

Proprietary agency banking

Digital financial services provided via the financial institution's own network of retail agents (branded under the financial institution’s logo/service name).

Third-party provider agent network

Digital financial services provided via a network of existing retail agents that are managed and branded under a third party's logo/service name.